So, You're Thinking of Investing in Regenerative Food Systems...

In Brief

The Regenerative Agriculture Initiative team at CBEY has looked inward and forward to show you how farming that boosts people, planet and profit can take root soon and broadly.

This series of articles by the Regenerative Agriculture Initiative team sets forth the opportunities, obstacles and obligations that define financing for regenerative agriculture in the United States, both before and in the coming recession.

This article details the second key lever: investing in regenerative farmland and farmers.

The traditional landscape of farmland ownership and financing in the United States has created barriers to the adoption of regenerative agriculture. Firstly, farmland is expensive. Farm real estate prices have doubled in the last decade. In 2019, cropland averaged $4,100 per acre and grew significantly more expensive closer to urban areas. Due to these high prices, most new and expanding farmers who do not have that kind of upfront capital have to rent land instead. In 2016, 38% of all farmland and over half of cropland was rented. Renting leaves farmers vulnerable to their landlord’s decision-making. Without a chance to reap profits, tenant farmers face a disincentive to invest in long-term regenerative strategies.

And short-term leases run counter to the economics that drive regenerative practices. These practices “take time to pay off. Leases are not set up to reward farmers for building soil health,” says Holly Rippon-Butler, Land Access Program Director of the National Young Farmers Coalition. “You’re not going to invest if the pay-off is ten years and you only have the land for three.”

As new and expanding farmers struggle to achieve land tenure, a significant transfer of farmland is forthcoming; 40% of farmland is owned by farmers above 65. But rather than transferring their land to new and expanding farmers, older farmers often need the sale of their land to fund their retirement. They thus are looking instead to sell to the highest bidder, often a developer or large, consolidated farm owner.

Investors are increasingly interested in entering this market, both to capitalize on this large transfer of land and to make decisions about who should manage it and how. Traditional investors see farmland as a stable asset that consistently rises in value and is uncorrelated with most mainstream asset classes, meaning it can mitigate the downside risk of their portfolios. Impact-oriented investors see an opportunity to achieve financial returns while improving environmental outcomes on the land and supporting farmer livelihoods. Innovative organizations, including impact-oriented farmland investment companies, food-centric credit unions, and local nonprofit chapters are building financial mechanisms to provide farmers with capital to expand their businesses and access land ownership.

This article will introduce the landscape of regenerative investment opportunities and dive into several unique farmland investment fund models that enable farmers seeking to pursue regenerative practices. This article will dive more deeply into regenerative farmland investment models because these models have received the majority of investment to date, they have the most direct exposure to agricultural land management, and they force stakeholders to consider thorny questions about future farmland ownership in the U.S.

The Regenerative Agriculture Investment Landscape

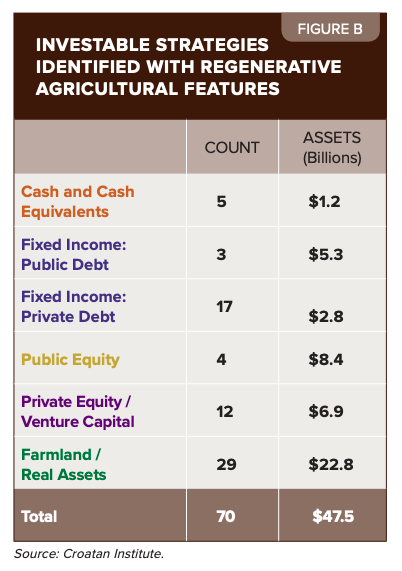

In July 2019, the Croatan and Delta Institutes, with the support of a USDA Conservation Innovation Grant, published a report analyzing the growing interest in regenerative food system investment. The report, Soil Wealth: Investing in Regenerative Agriculture across Asset Classes, quantifies the US landscape of investment in sustainable and regenerative agriculture. Soil Wealth identifies $321.1 billion in managed assets that explicitly integrate sustainable food criteria in their investment strategies, and a smaller subset of investments - $47.5 billion - specifically related to regenerative agriculture (see Figure B).

Soil Wealth provides recommendations for investors in each asset class, categorizing mechanisms based upon their level of maturity. Some finance ideas have not yet been applied, while others direct capital to established tried-and-true approaches. The report suggests that emerging asset classes that are most ripe for rapid development are farmland, cash and fixed income.

The report asserts that “farmland naturally provides the most direct way to enable regenerative agriculture in the field.” In the fixed income and cash markets, rural banks, credit unions, private loan funds, and state governments “can develop targeted lending and financial services to farms and businesses within the regenerative agricultural value chain as well as depository products for investors seeking exposure to regenerative agriculture.” Seed-stage initiatives identified by the report in the cash and fixed income markets include:

-

Cash & Cash Equivalents: Specialized Credit Union: The Maine Harvest Federal Credit Union is the first credit union in the country to lend exclusively to farmers and food entrepreneurs with a mission of boosting the agricultural economy and increasing farmland access. The Credit Union partners with the Maine Farmland Trust and the Maine Organic Farmers and Gardeners Association.

-

Public Bond Market: Apply Existing Ag Bonds to Regeneratie Farmers: Aggie Bonds are private-public loan programs that help new farmers purchase farmland and equipment by offering below-market interest rates. While only five states currently issue Aggie Bonds, the program could be modified to invest in new farmer recipients who practice regenerative agriculture.

-

Private

(1) A financial obligation to another person or entity; (2) An obligation which is created by borrowing; or (3) The sum of all of the financial obligations of a person or entity.

Market: Pairing Technical Assistance with Financing: The Carrot Project is a nonprofit organization that pairs technical assistance with financing and business management services to increase the number of successful small farm and agriculture businesses. The organization aims to increase local food production across the Northeast by offering specialized training, personalized assistance, and peer networking to small and mid-sized farms and food processors.

Private

(1) A financial obligation to another person or entity; (2) An obligation which is created by borrowing; or (3) The sum of all of the financial obligations of a person or entity.

Market: Pooled Loan Funds: The non-profit Slow Money Institute coordinates local slow money networks to catalyze the flow of capital to local food systems, farmers, and food enterprises. Slow Money networks organize 0% and low-interest lending, pitch fests, and on-farm educational events.Farmland Investment Companies

Farmland investments are by far the largest asset class in the regenerative financing ecosystem, representing almost half of assets under management. Investors are drawn to this asset class because farmland yields reliably positive financial returns while offering helpful diversification and powerful opportunities for impact.

The RAI chose to highlight the four farmland investment groups below as some of the best existing models seeking to achieve regenerative outcomes. Each demonstrates a unique approach to extracting financial value from land managed for environmental and social outcomes. RAI identified these groups through the Soil Wealth report, presentations at the Regenerative Food System Investment Forum 2019, and classroom presentations at Yale School of Forestry & Environmental Studies. RAI gathered further information through interviews with Alex Mackay at Iroquois Valley Farmland REIT, Esther Park at Cienega Capital, and Jacob Israelow and Benneth Phelps at Dirt Capital.

While some of these companies operate properties themselves and receive annual income based on agricultural yields and price premiums (often through certifications like USDA Organic), others lease or sell land to independent farmers, and receive returns based on annual lease and mortgage payments. These entities generally expect an annual appreciation in land value of around 5 or 6% plus any annual cash flow returns from leases, mortgages, or yields. Those yields vary depending on the year and the fund model. The models described below vary across returns and across their impacts on agricultural landscapes and communities.

Case One: Dirt Capital Partners

Dirt Capital Partners structures their investment vehicles similarly to real estate private equity funds, a partnership set up to raise equity for ongoing real estate investment. Investors who can bear some risk place capital with the firm, expecting returns from a variety of farmland investment projects. The company has made 24 farmland investments among three funds since 2014, all in the Northeast and Mid Atlantic regions.

The investments all support farmers with viable business models to obtain secure access to land and a pathway to ownership. Dirt Capital invests in farm properties with and for a specific farm business. Most transactions are long-term leases with a fixed price option for the farmer to buy after nine years and an early option after five years. Dirt Capital charges a cost of capital to farmers of around 7.5%. This is often structured with average annual lease payments of 5-6% and land appreciation of 1-3% fixed for the farmer’s purchase option. The funds do not have an explicit hurdle rate for investors. Most investors in the funds are impact-first, mission-aligned family offices and foundations.

Dirt Capital sorts its deals across four goals:

- Land access for younger farmers: Dirt Capital works with young farmers that have established viable businesses and seek secure land tenure, but don’t yet have the capital to buy property themselves. Through long-term leases with Dirt Capital, young farmers can build up the capital and collateral to be able to make a down payment on the property with a local lender at the end of the lease. In some cases, these projects involve transferring land from retiring farmers to beginning farmers.

- Expansion projects to help established farms scale up: Dirt Capital also works with established mid-career farmers who own their “home farm” and are seeking long-term access to adjacent land to grow an already successful business. Sometimes a neighbor’s farm is available and it is a once-in-a-generation opportunity to expand on adjacent land; in other cases, farmers seek additional land in part to support the entry of their children into the business.

- Complex land deals: Dirt Capital was founded by Jacob Israelow, whose background is in commercial real estate structuring and transactions. The fund brings both expertise and upfront capital to complicated land deals that involve many stakeholders, including farmers, conservation groups, local governments, and businesses, and create innovative arrangements that mitigate and appropriately distribute risk.

- Conservation financing: Dirt Capital works with local land trusts to establish conservation easements on properties in order to lower the land price when farmers have the option to buy. As funds from an approved easement can take years to receive, it is difficult for farmers to establish a conservation easement on a new property themselves, because they would have to first buy the property at full cost with upfront capital before selling the conservation easement.

One investee operates within 60 miles of New York City. That’s Fishkill Farms in East Fishkill, NY, a diversified, organic fruit, vegetable, and egg operation that uses “beyond organic” practices. The farm is surrounded by suburban development.

Dirt Capital partnered with the Scenic Hudson Land Trust to purchase 345 acres of farmland, woodlands, and wetlands adjacent to Fishkill Farms that was at risk of potential subdivision and housing development. Fishkill Farms leases the agricultural portion with an option to buy at the end of the long-term lease. A conservation easement will bring down the cost to buy the property for the farmers, and protect the property’s vital recreational and ecosystem values.

Case Two: Farmland LP

Farmland LP acquires undervalued farmland and adds value through implementing sustainable management plans that include organic certification, infrastructure, and increasing crop diversity. Their stated goal is to “demonstrate that large-scale sustainable agriculture is more profitable than the dominant model of commercial agriculture in the U.S. today.” Founded in 2009, Farmland LP bought their first farm in 2010 and now manages over 12,500 acres in northern California and Oregon.

According to their 2017 Impact Report, Farmland LP’s farm management decisions subscribe to three core values:

- Regenerative, not extractive - enhancing soil biota, building topsoil, improving fertility and integrating biodiversity

- Business ethics to match land ethics - adhering to B-Corp certification standards

- A positive example - demonstrate a positive, replicable example of producing healthy food on healthy land

For its current Vital Farmland REIT, Farmland LP targets an 11.1% return for investors. This fund owns 8,711 acres, with $81 million in assets invested and a goal of $150 million total investment. Their first fund, which closed in 2014 neted a 9.6% IRR.

Though Farmland LP does not share case studies on their investments publicly, they do share information on their measurement of the ecosystem impact of their management practices. In 2018, they partnered with the Delta Institute and Earth Economics on a USDA-funded study of Farmland LP’s organic and regenerative agriculture practices.

The study showed that over 5 years on 6,000+ acres of managed land, their property generated $21.4 million in “ecosystem service value benefits” from the restoration of clean water, pollinator habitat, and healthy soils. For example, after acquiring land that had received heavy pesticide applications on alfalfa and corn, Farmland LP recognized the need for re-establishing pollinator habitat in order to transition the land to organic practices in the future. They installed 2,700 feet of hedgerows along fields at Brentwood Creek Farm in California. Farmland LP calculated that the ecosystem service value of planting these native shrubs to provide pollinator habitat was $19,000/year/acre.

Case Three: Iroquois Valley Farmland

Iroquois Valley is a Farmland Real Estate Investment Trust (REIT), meaning that it pays out income in dividends to shareholders. It raises capital from private impact investors and individuals and then secures land for organic farmers who want to establish or expand organic farms. Staff say they design innovative leases and mortgages. The company’s portfolio now totals approximately $55 million across 14 states, mostly in the Midwest and Great Lakes regions.

One unique aspect of the company’s structure is that REITs are required to have a broad base of ownership, so there cannot be a concentration of the company’s shares in the hands of a few investors or the company will lose its tax-exempt status. Iroquois Valley has approximately 400 shareholders and another 100 noteholders whose investments average $100,000 and range in size from $10,000 to $5 million.

Financial Performance:

Investors that invested capital in the REIT at its inception, about nine years ago, have received an annualized return of 9.31%. However, those who invested three years ago, have only seen an annualized return of 1.76%. This range of returns is attributed to many factors, including the recent stagnation of farmland values, international grain prices (grain makes up most of the portfolio) and the lack of organic farmland valuations independent of conventional land. Alex Mackay, Director of Business Development and Investor Relations at Iroquois, also indicated that investments in farmland should normalize over time.

“The history of farmland investment in the US indicates that the longer you can stay invested, the more likely you will see returns normalize and offer the incremental growth and non-correlation that makes this investment class attractive in the first place, said Mackay.

Example:

Villicus Farms, a 7,400 acre organic property in the Northern Great Plains of Montana owned by farmers Anna Jones-Crabtree and Doug Crabtree, grows a variety of heirloom grains and legumes, including emmer, spelt, kamut, oats, lentils, and flax. The fields are divided into 240 foot-wide cultivated segments.separated by 20-30 foot conservation buffers. The Crabtrees planted native wildflowers and grasses on the buffers to support biodiversity, increase water holding capacity, and reduce wind erosion. They say that the soil organic matter content on their fields has increased an average of 3.2% each year. Iroquois Valley has bought property and set up long-term leases for Villicus Farms three times, each time to help them continue to expand their operations. The first was for 320 acres in 2016, then for an additional 960 acres in 2017, and finally for an additional 2,200 acres in 2019.

Case Four: Cienega Capital

Cienega Capital is a single-family office impact investment fund. The family that endowed it also runs a ranch education center, Paicines Ranch. With the Globetrotter Foundation, the organizations finance what they call “The No Regrets Initiative.” The collective vision for these initiatives is to regenerate agricultural soils and communities throughout North America. As of December 31, 2019, Cienega has invested over $13.5M, approximately distributed as 47% in working capital, land, and equipment loans, 17% in equity (including an organic seed company and grass-fed beef aggregator), 10% in like-minded funds, and 14% in a joint land venture with a rancher.

The No Regrets Initiative puts on an annual Learning Journey that invites investors and philanthropists to take a deep dive into regenerative agriculture through field analysis and case studies.

Financial Performance:

Cienega Capital’s returned capital to date has achieved an ROI of 4.46%-which suits the investors just fine. “We don’t let the financial return profile drive our decision-making in any way,” says CEO Esther Park. The loans they provide carry an annual interest rate in the 5-6% range. Though the family office is highly impact oriented, they don’t want to offer loans at an excessively low rate because it might negatively impact farmers’ long run economic sustainability.

“My philosophy around that is I don’t want to do anybody any disservice...by giving someone super concessionary money, which may make it difficult for them to cope with financing from traditional sources later on,” Park explained.

On the equity investment side, Esther described a radical mindset. Rather than focusing on companies expected to succeed, the fund has a bias towards innovation and learning.

“There have been cases where we have invested in companies, largely anticipating we will lose the investment,” explained Park. “We do that because progress is made only when mistakes are made. If we are going to push forward this field of economically viable regenerative agriculture businesses, in some cases you have to invest in models that have a high likelihood of failure because the field will learn something from that and that is information for the next group of entrepreneurs that will improve. Unless someone takes that risk, that progress won’t be made.”

For example, investee Oshala Farm, a young herb farm in Oregon, had borrowed money for an irrigation system, tools, and an upgraded greenhouse on terms that required repayment within a year. At the end of the year, the farmers had made their income from herb production, but in paying back the loan burned off any working capital they would have had to invest in next year’s growing season. Cienega Capital stepped in to properly finance the equipment with a term loan with a longer repayment timeline, freeing up working capital for the farmers to invest in the following year’s production.

Important Considerations for Investors

When investors choose between funds or when wealthy families set up their own impact-driven funds, they are signing up not only for different levels of risk and return projections, but also for different visions of the future of agriculture. Do investors want to expand the land owned and managed by investment companies or land owned and managed by independent farmers? Will they take risks on innovative agricultural entrepreneurs that are likely to fail or will they stick to businesses most likely to succeed?

An important piece of this conversation is who will benefit from these funds. As described above, most new and beginning farmers face financial barriers to land access. On top of that, farmers of color and other marginalized groups face further difficulties caused by structural racism, from discriminatory laws and funding to denied reparations and labor protections. In part due to this history, according to research by Megan Horst and Amy Marion, farmers of color are “more likely to be tenants than owners... and generated less wealth from farming than their white counterparts.” In fact, white people own 98% of farmland in the United States.

In addition, farmers of color, female farmers, indigenous farmers, and immigrant farmers, who typically manage smaller farms with higher-value products, receive significantly less government funding and support. It is thus important to consider how structural racism might affect farmland investment fund models.

“What happens if a Black farmer in Selma loses their land because they can’t get loans to run a cotton crop this year and then a regenerative farmland investment firm invests in that land and leases it to a 25-year-old from Atlanta who’s excited about regenerative agriculture?” asks Stephen Wood, an applied scientist at The Nature Conservancy. “That seems like a deeply problematic possibility of land gentrification, even if right now it’s a slight possibility.”

“If these funds aren't explicitly addressing equity, then they are likely contributing to inequality,” added Rippon-Butler.

One of the four tenets of regenerative agriculture laid out by the RAI and other stakeholders is “healthy communities.” As these funds seek to achieve regenerative outcomes on the land and support farmer livelihoods, they might consider who is benefiting from investment and what socially and racially equitable farmland investment might look like. This is not easy work, and there are structural barriers in place. As described above, most farmers of color and female farmers manage smaller plots of land. Given the amount of time and resources that go into setting up an investment deal, it may be financially infeasible for investment companies to work on smaller deals with these farmers.

“The due diligence and underwriting process for a deal of any size takes considerable time and resources for an investment company, so it follows that the more capital you allocate, the more revenue you are creating for the investors down the road,” explained Alex Mackay of Iroquois Valley. “That traditional fund approach doesn't always consider the amazing array of impacts you can achieve by pursuing smaller deals.”

While investment funds are powerful tools for change, they cannot solve the land access issue on their own, and they are often only accessible to accredited investors. The Soil Wealth report details a number of alternative emerging financial mechanisms for supporting regenerative farming that allow anyone to participate, work on a variety of scales, and seek a wide diversity of outcomes.

As many of these vehicles remain in their seed stage and are likely to be implemented at local and regional scales, regenerative agriculture stakeholders have plentiful opportunities to support and help formulate these efforts. Budding investors, non-profit managers, food industry professionals, or others, can join a local Slow Money chapter, credit union, or mission-aligned bank and advocate for how and to whom they want their money to flow.